SINCE the Covid-19 pandemic broke out in late 2019, the costs of most commodities have moved north, which was evident in 2021 with the Bloomberg Commodity Index (BCOM) — which tracks 23 power, metals and agriculture futures contracts — hitting a 10-year excessive of 105.84 in October.

In contrast with a yr in the past, and as much as Dec 17, the index has surged 25%. ING head of commodities technique Warren Patterson and senior commodities strategist Wenyu Yao say in a December observe to buyers that recovering demand following Covid-19, provide chain disruptions, authorities coverage and hostile climate have all contributed to tightening in markets this yr, which has propelled costs increased.

“Going into 2022, we anticipate the disruptions we’ve seen in provide chains to enhance, whereas the balances for a number of commodities will look much less tight than in 2021. This could imply that costs edge decrease from present ranges. However, importantly, we nonetheless anticipate them to stay above long-term averages.

“So total, whereas we see some marginal draw back dangers throughout the commodities advanced in 2022, on a historic foundation, costs are prone to commerce at elevated ranges for an additional yr. The important thing danger, after all, is the coronavirus pandemic. Total, we’re preserving the religion,” they wrote.

Whereas metals akin to gold and iron ore had a stellar efficiency final yr, their efficiency in 2021 was muted compared. Nevertheless, it was an excellent yr for power, with surging costs in crude oil and pure gasoline, in addition to for agricommodities, with the costs of wheat and low trending upward. The costs of crude palm oil (CPO) — an agricommodity that isn’t a part of the BCOM however one which is significant to Malaysian exports — additionally surged to new highs.

We check out the efficiency of crude oil and CPO in our accompanying tales. Right here, we revisit the efficiency of among the different commodities, and try their outlook for the approaching yr.

Surging pure gasoline costs

In contrast with a yr in the past, spot Asian LNG (liquefied pure gasoline) costs measured by the Japan-Korea marker (JKM) have greater than tripled yr on yr to US$45 per metric million British thermal unit (MMBtu).

ING’s Patterson says spot Asian LNG has largely traded at a wholesome premium to that of Europe, with pure gasoline costs in Europe surging on account of tight inventories, and subsequently there was a transparent incentive to ship cargoes into Asia.

“China’s LNG imports are up 23% yr on yr over the primary 10 months of the yr, and have overtaken Japan this yr to be the world’s largest importer [of LNG]. Chinese language demand has been supported by sturdy industrial demand together with rising demand from the facility sector. China’s ambitions for [carbon] emissions to peak earlier than 2030 ought to proceed to show supportive for LNG demand within the coming years,” he says.

Reuters reported in June that state-owned enterprise China Nationwide Petroleum Corp (CNPC) expects China to chop its coal use to 44% of power consumption by 2030 and eight% by 2060 because the nation goals to make use of extra pure gasoline to realize its local weather change targets.

“Wanting on the ahead curve, the Asian market is at a premium to Europe all through 2022, with the premium being at its widest early subsequent yr. Subsequently, don’t anticipate the [Asian] LNG market to unravel Europe’s tightness. The area might want to proceed to compete towards Asia for spot LNG by 2022,” says Patterson.

OCBC Financial institution economist Howie Lee says LNG costs have remained closely elevated in Europe and Asia, with each the TTF (Title Switch Facility) — a digital buying and selling level for pure gasoline within the Netherlands) and the JKM buying and selling in extra of US$30/MMBtu as at December this yr — greater than double the value traded at the beginning of the yr.

Nevertheless, he expects LNG costs each in Europe and Asia to return to US$25 per MMBtu by the tip of subsequent yr.

“Whereas that represents a year-on-year decline, it stays considerably elevated by historic requirements,” he says.

Muted efficiency from metals

Gold costs, which began out the yr peaking at US$1,950 per ounce in January, have since retreated to as little as US$1,683.54 in March on the again of a strengthening US greenback. In contrast with a yr in the past, gold costs have declined 4% to US$1,802.41 per ounce on Dec 17.

OCBC’s Lee expects gold to pattern decrease subsequent yr, at a mean of US$1,500 per ounce.

“Most central banks have now listed taming inflationary pressures as one in every of their core priorities in 2022, which suggests the worldwide rate of interest surroundings is prone to tighten sharply on mixture subsequent yr. The aggressive tempo of charge hikes could outweigh demand for gold as an inflation hedge, leading to a web bearish impact on gold,” he says.

Fitch Options, in its commodities outlook report, additionally sees gold costs averaging decrease in 2022, because the dollar strengthens and bond yields proceed to get well.

“We see costs averaging US$1,700 per ounce in 2022 with continued bouts of volatility, in contrast with our forecast of US$1,800 per ounce for 2021. Gold will stay supported within the close to time period as inflation runs at a multi-year excessive, which is able to preserve the enchantment of gold. Nevertheless, this shall be balanced by rising dangers of the US Federal Reserve elevating rates of interest at a sooner and stronger tempo than at the moment anticipated by market members,” says Fitch.

Iron ore costs, which had an outstanding run in 2020, noticed a drastic decline this yr. Costs had peaked in Might at US$227 per tonne following the suspension of the China-Australia Strategic Financial Dialogue, which led to Chinese language metal mills speeding to pile up provides within the occasion of potential commerce restrictions between the 2 international locations.

Nevertheless, iron ore’s fortunes rapidly turned and costs headed south, hitting the bottom level this yr at US$86 per tonne in November, on the again of dismal demand outlook for metal merchandise and uncooked supplies in China.

“Decrease metal manufacturing has did not elevate metal mill margins in China, which had turned detrimental within the fourth quarter of 2021 as a result of weaker demand from the downstream property sector and slower exercise from others owing to frequent energy shortages.

“The China coverage panorama on the macro degree, together with strikes towards decarbonisation, stays a cap over the medium-term demand outlook for iron ore. As such, China’s metal manufacturing is unlikely to return to the degrees seen within the first half of 2021,” says ING’s Yao.

ING expects iron ore costs, which have been buying and selling at US$118 per tonne on Dec 17, to pattern decrease in 2022, averaging US$100.

“On common, we anticipate costs to slip to US$100 per tonne over 2022, with the primary upside dangers nonetheless being potential provide chain disruptions in gentle of the Omicron variant,” says Yao.

Copper costs quoted on the London Metallic Change however have elevated 19% yr on yr (y-o-y) to US$9,437.5 per tonne.

OCBC’s Lee expects copper costs to peak additional at a mean of US$12,000 per tonne subsequent yr.

“Copper demand is anticipated to enter its second yr of enlargement, particularly after the not too long ago concluded COP26 (2021 United Nations Local weather Change Convention) demonstrated an rising willingness by governments to prioritise clear power. Unresolved provide chain bottlenecks, which can persist till the second half of subsequent yr, are additionally anticipated to maintain costs supported,” he says.

LME tin costs have surged a whopping 94% y-o-y to US$38,840 per tonne. Costs had earlier reached a document excessive of US$41,073 per tonne in November. Malaysia Smelting Corp Bhd, the world’s third largest producer of tin, attributed the document tin worth to the present world panorama of selling environmental and sustainability initiatives, photovoltaic installations, electrical automobiles and progress in electronics, which bodes nicely for the demand for tin.

Fitch Scores, which expects tin costs to ease barely from spot ranges to US$32,500 per tonne subsequent yr, says tin is anticipated to stay on a agency upward pattern within the coming decade to achieve US$35,500 by 2030 — practically double its common worth of US$18,729 per tonne from 2016 to 2020.

“We anticipate tin demand to proceed outstripping provide, pushing the market into deficit by 2026. On the provision aspect, a skinny pipeline of tin mining initiatives will tighten the tin focus market, resulting in elevated competitors amongst smelters and constrained ore feed for refined output progress.

“On the demand aspect, the worldwide use of tin will improve quickly by the steel’s use in electronics (particularly as electrical automobiles more and more include better quantities of electronics of their physique) and photo voltaic panels (in photovoltaic cells), cementing tin’s standing as a commodity of the long run. In the end, this can enable the market to tighten and return to a manufacturing stability deficit by 2026, which is able to solely develop deeper over time,” says Fitch.

Agricommodities surge

Wheat costs have surged 25% y-o-y to US$7.72 per bushel on Dec 17, because of a collection of droughts and heatwaves round wheat-producing areas.

“Export taxes have been additionally launched and later raised in Russia, a key exporter, at a time when importing international locations have been competing for accessible wheat,” says Rabobank in its Agri Commodity 2022 Outlook Report.

Rabobank expects wheat costs to pattern increased in FY2022, at US$8.10 per bushel within the second quarter of 2022, earlier than moderating to US$7.50 within the fourth quarter.

“Our base case for 2022/23 reveals a small surplus within the world stability sheet after two years of deficits, however it is going to take greater than half a yr for this to materialise. Regardless of wonderful costs, manufacturing is anticipated to extend solely marginally, and will probably be the drop in demand for feed wheat that can enable that surplus to emerge,” says Rabobank.

Espresso costs had an outstanding run in 2021, with Arabica espresso costs rising 85% y-o-y to US$2.35 per pound on Dec 17, as a result of logistical points such because the scarcity of containers that led to panic shopping for of the commodity.

“Panic shopping for is prone to be alleviated after Christmas, permitting costs to drop,” says Rabobank, which expects Arabica espresso costs to drop to US$2 per pound within the first quarter of 2022, earlier than retreating to US$1.66 within the fourth quarter of subsequent yr.

ING’s Patterson expects Arabica espresso costs to common round US$1.95 per pound in 2022.

“Demand is anticipated to outstrip provide. This shall be pushed by a mixture of additional progress in demand, together with a Brazilian crop weighed down by frost and probably drought. Nevertheless, a lot will rely upon precipitation within the coming months. There are some who’re forecasting a deficit of as a lot as seven million baggage. The expectation of a deficit [next year] and the uncertainty on how massive this deficit could possibly be recommend that costs ought to stay nicely supported,” he says.

In the meantime, cocoa costs have elevated by 6% yr on yr to US$2,547 per tonne on Dec 16 because of anticipated decrease manufacturing. Rabobank expects cocoa manufacturing to say no in 2022 because of decrease enter and poor climate at the beginning of the season, and forecasts costs to pattern barely increased at US$2,580 per tonne in Q1 2022 earlier than additional rising to US$2,710 per tonne in 4Q2022.

A document yr for palm oil costs

By Supriya Surendran

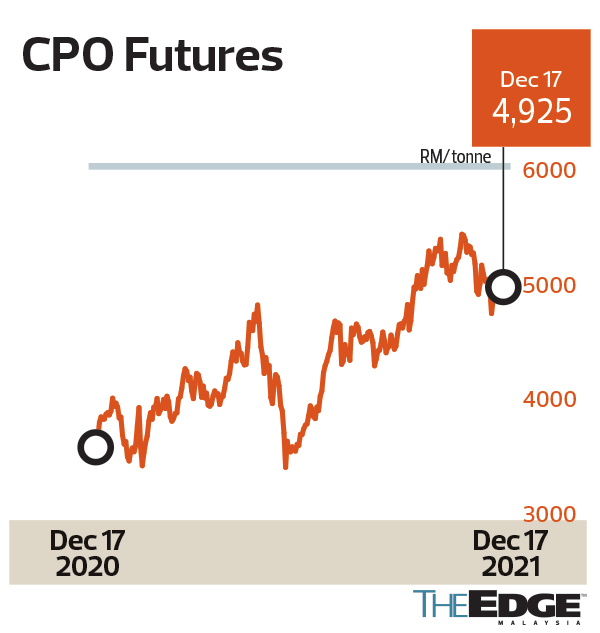

A document yr for crude palm oil (CPO) costs — that’s one of many financial positives 2021 shall be remembered for, with CPO futures surging to an all-time excessive of RM5,446 per tonne in November on the again of tight edible oil provides. As at Dec 17, the value of CPO was RM4,925 per tonne, a rise of 37% from a yr in the past.

Rabobank in its agri commodity outlook report says palm oil costs shall be supported by the expectation that world vegetable oil inventories will stay in deficit subsequent yr.

“The mix of a less-than-optimal palm oil manufacturing improve and minimal year-on-year biodiesel demand improve in 2022 in Southeast Asia will lead to a slight surplus scenario for palm oil globally in 2022,” it says.

Rabobank notes, nevertheless, that the y-o-y lower in world tender oil inventories subsequent yr shall be bigger than the rise in palm oil inventories. It attributed this to “an expectation of accelerating y-o-y world soy oil demand” amid rising demand from the renewable diesel trade and decrease y-o-y world rapeseed oil manufacturing.

Rabobank expects CPO costs to pattern decrease at RM4,700 per tonne within the first quarter of 2022 (1Q2022) earlier than additional declining to RM4,300 per tonne in 4Q2022.

CGS-CIMB Analysis in a Dec 12 observe to purchasers says CPO costs might stay excessive till 1Q2022 earlier than trending decrease when palm oil provide recovers and crushing actions of oilseeds enhance.

“The sturdy CPO worth and expectations of a gradual return of overseas staff are optimistic [points],” it explains, although additionally noting, “These are offset by considerations over rising fertiliser prices.”

CGS-CIMB expects CPO costs to commerce at RM3,600 per tonne in 2022.

Dr Sathia Varqa, proprietor and co-founder of Palm Oil Analytics, a Singapore-based unbiased, on-line writer of palm oil market information, thinks costs ought to begin easing from March 2022 as manufacturing improves, “based mostly on the belief that there isn’t any main climate disruption and staff are prepared for harvesting [work] in Might”.

Sathia expects the CPO futures lively month contract to pattern at RM4,200 to RM4,400 per tonne this month earlier than buying and selling increased in January and February subsequent yr.

“Costs are anticipated to decrease once more from the tip of March 2022 onwards to RM3,900 to RM4,200 per tonne,” he tells The Edge.

OCBC economist Howie Lee sees palm oil buying and selling at a mean of RM4,750 per tonne subsequent yr, with manufacturing anticipated “to return in earnest subsequent yr in each Malaysia and Indonesia”.

Additional, “our expectations of upper soy costs imply the palm advanced can also be anticipated to be lifted increased.”

Soybean oil, a costlier various to palm oil, has seen a 50% improve within the worth of its futures contract to US$0.54 per pound.

Rabobank says within the US, biodiesel demand progress has been overwhelming, with soybean oil being its main feedstock.

“Sturdy biodiesel costs, Covid-19 convalescence and provide dangers present assist for soy oil to stay [at] document highs within the yr forward,” it says.

Rabobank expects soybean oil to commerce at ranges of US$0.60 per pound in 1Q2022 earlier than moderating to US$0.58 per pound in 4Q2022.

Esta nota fue traducida al español y editada para disfrute de la comunidad Hispana a partir de esta Fuente